Sterling’s ‘Rollout’ Resurgence

23 February 2021

A beautiful (rates) rise

9 March 2021INSIGHT • 2 March 2021

Why Bitcoin matters (to us)

Kevin Lester, CEO

We traded about a third of a trillion dollars at Validus in 2020, across 55 different currency pairs. None of that was in Bitcoin. Despite lacking any direct exposure to crypto, I believe that understanding the Bitcoin phenomenon is essential to understanding our current macro environment and the significant challenges that lie ahead for the global monetary and financial system.

Bitcoin is 100% faith. Come the next market phase where faith is at a minimum, what do we think will happen to a stock whose entire reason for existence is faith and nothing but faith?

Jeremy Grantham, Co-founder and CIO, GMO, February 2021

…people believe that the United States currency is perfectly reliable and stable in value…

Jerome Powell, Federal Reserve Chair, February 2021

Her shares, however, were going up. Gambling on the stock exchange had become the fashion – the only way to avoid losing all one’s money and perhaps to add to it.

‘When Money Dies’, Adam Fergusson, 1975

Bitcoin Gold

Russel Okung, Carolina Panthers, February 24th, via Twitter

When Russel Okung, left tackle for the NFL’s Carolina Panthers, elected to take half of his $13 million salary in Bitcoin, no one expected this decision to make him one of the highest paid players in the entire league. But that is exactly what has happened, with the veteran offensive tackle out-earning global superstars such as Tom Brady and Aaron Rodgers.

The Okung story is more than an interesting piece of sports trivia – it is symbolic of the growing doubts surrounding the sustainability of the US dollar-centric global monetary system – when the US fiscal deficit exceeds 17% of GDP and the Fed expands its balance by as much in a few weeks as it did in the five years following the last global financial crisis in 2008 ($3 trillion).

According to author and independent macro strategist Russell Napier, the total amount of US dollars in the world is up by 25% year-on-year. And this is not just a US phenomenon – the amount of euros has increased by 13.5%, sterling and Canadian dollars by 12%, and so on.

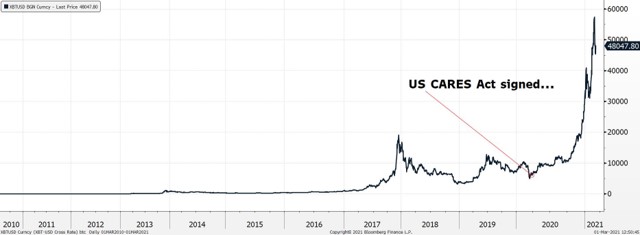

This combination of global fiscal profligacy and a rapidly increasing money supply has, quite reasonably, led to growing concerns about inflation risk. In our 2021 Global Macro Outlook we posited three scenarios for global markets: 1) benign reflation (40%); 2) market meltdown (20%); and 3) market melt-up (40%). It is this third scenario which is currently worrying the markets, with bond yields pushing higher and the US dollar proving stubbornly resilient (as we predicted would happen under a ‘market melt-up’ scenario). Which brings us to the question of why Bitcoin (and, more precisely, the price of Bitcoin) matters. First and foremost, you can look at the price of Bitcoin as an expression of distrust in the current monetary system; BTC = short Modern Monetary Theory (MMT). It is not a coincidence, in our view, that the parabolic rise in the price of Bitcoin began at precisely the moment when the CARES act ($2.2 trillion) was signed into law.

Chart 1: Bitcoin’s price since inception

In other words, Bitcoin’s surge signals that risks are building in the global financial system. But what if Bitcoin is just a bubble? A recent analysis from Deutsche Bank shows that Bitcoin’s rise makes it the third biggest financial bubble in history, after the Dutch tulip mania (1637) and the Mississippi bubble (1720), and just ahead of the South Sea bubble (also 1720).

Leaving aside the question of whether Bitcoin is in fact a bubble (many would argue its rapid price rise is justified), if Bitcoin’s risk is a sign of financial instability, can we assume that a declining price is a good thing?

Unfortunately not, at least not anymore. One of the side effects of Bitcoin’s price rise is that it has become a systemically important asset class. The market capitalization of Bitcoin itself is approaching $1 trillion (about 1/10th of that of gold), and the total crypto complex has a market capitalization of close to $1.5 trillion.

Coinbase, the largest crypto platform in the US, filed for a direct listing on the Nasdaq this week, which is expected to value the company at about $100 billion, which is about the same valuation as Goldman Sachs. In Canada, the first publicly traded Bitcoin exchange-traded fund (ETF) was launched last month and collected over $400 million in assets under management in two days.

An article in Institutional Investor magazine in 2018 asked the question: ‘Would Bitcoin at $50,000 put the global systemic-risk watchdogs on high alert?’ Whilst not answering the question directly, it does quote Agustin Carstens, head of the Bank of International Settlements (the ‘Central Banker’s Central Bank’) as saying: ‘if authorities do not act pre-emptively, cryptocurrencies could become more interconnected with the main financial system and become a threat to financial stability.’

With Bitcoin now trading at or around the $50,000 level, the questions of Bitcoin’s systemic risk are no longer hypothetical – there is little doubt that crash lower, say below $10,000, would risk a degree of financial contagion.

While many of us may not (yet!) trade Bitcoin, at least professionally, there is little doubt about its importance to global financial markets. In fact, in our recent Linked-In poll, Bitcoin tied with gold as the best hedge against inflation (both were the choice of 42% of respondents). Not bad for an asset class with barely a decade’s track record, when you consider that gold has been used as money since 550 B.C.! Whether you love it or hate it, you can no longer ignore it.

Be the first to know

Subscribe to our newsletter to receive exclusive Validus Insights and industry updates.