Treading the inflation tight rope: can the BoE keep its balance?

17 May 2022Central Bankers Spark Further Inflation Fear

27 May 2022INSIGHT • 24 MAY 2022

Policy Mistakes, Sticky Inflation and Higher Rates

Shane O'Neill, Head of Interest Rate Trading

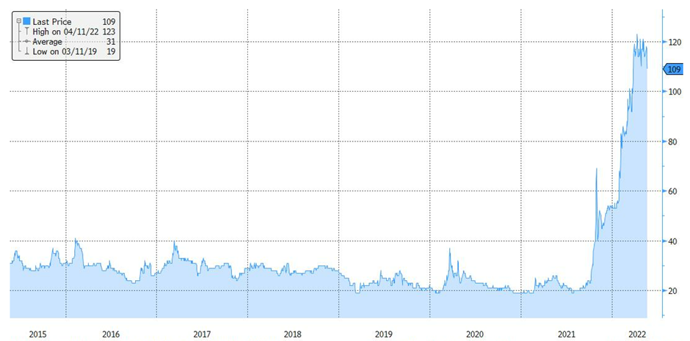

Chart 1: After languishing for much of the last decade, interest rate volatility is back and potentially here to stay

Source: Bloomberg

The outbreak of Covid, and governmental reaction to it, left Banks with little choice than to let go of forward guidance and act quickly. Cutting rates and ramping up QE with incredible speed. The Fed almost doubled the size of its balance sheet in the second quarter of 2020 and continued to print money well into 2022. Cautious not to derail the economy and reverting to old habits, forward guidance again took hold. The Fed at first wrote off inflation as “transitory”, but even once they accepted the stickiness of the current wave of inflation, they made it clear that hikes wouldn’t occur until after the end of QE and that QE reduction would be gradual. So hooked were the markets on forward guidance and QE, that even the concept of hiking “immediately” after ending QE caused concern – last time the Fed tapered QE the market had a year to digest it before the first hike.

Chart 2: The Fed continued to grow their balance sheet well after it became clear that inflation wasn’t “transitory“

Source: Bloomberg

Sticky, Broad Based Inflation

But that was in a different inflationary environment – CPI during this period was at or below 2% – now is different. As early as September last year there were rumblings that Covid driven inflation may not be as transitory as hoped – prices were being driven higher by both supply and demand side factors. In early December, the term “transitory” was officially retired by both Chairman Powell and Treasury Sec. Yellen, and yet the printing presses kept rolling. So, despite growth bouncing back, unemployment at 3.9% (near historic lows) and inflation (now accepted as broad based and sticky) at 7%, the Fed continued to print money and keep rates at historic lows for a further quarter – adding some $300bio to their balance sheet.

The Fed weren’t alone, the reaction functions of the BoE and ECB were also slow, and this policy error has helped put us in the position we are now. Inflation is increasingly broad based and printing multi decade highs across the developed world. In the US, recent numbers have shown worrying increases in rent and food prices and in the UK, we have inflation at 40y highs being driven by everything from fuel to furniture. On the back of recent numbers, rhetoric from the banks is starting to shift and become even more aggressively hawkish. Powell has suggested the Fed “won’t hesitate” to take rates beyond neutral if needed, and ECB member Knot hinted that moves of 50bps are in play, a marked escalation from a bank which has moved in 10bps increments since 2014.

Path Ahead

The scenario all central banks would love to engineer from here is an economy with marginally higher interest rates, bringing inflation under control but avoiding a hard landing – unfortunately, their hesitation has made this outcome increasingly unlikely. For risk managers and investors alike, the risks seem clear – inflation, now embedded, refuses to retreat in the face of ever-increasing rates. The market pricing of “neutral” rates is off the mark – inflationary pressures from deglobalisation and supply issues, worsened by resurgent East/West tensions, means that we are back in a higher rate environment where “normal” is again 4-5%, not the 0-1% we have seen for the last decade.

Whether the above plays out and rates persist at elevated levels for an extended period or not, if inflation remains sticky, central banks will have to move faster and perhaps wean markets off their meticulous forward guidance. Recency bias is hard to overcome, and it is tempting to assume rates won’t move too much higher from here, but this needn’t be the case. If your business or investment works with rates where they are today, there’s an increasingly compelling argument to take rates risk, and the incoming volatility, off the table as we march toward a period of economic fragility.

Be the first to know

Subscribe to our newsletter to receive exclusive Validus Insights and industry updates.