Canada at the Crossroads – Potential Market Implications of the 2025 Federal Vote

1 April 2025

A tariff tale: Britain’s partial pardon in Trump’s tariff blitz

9 April 2025INSIGHTS • 03 April 2025

“Liberation Day” - Post event update

Louis Sangan, Global Capital Markets, Senior Associate

Riding the tariff storm in global markets

What was a highly anticipated event did not disappoint – and now the dust has settled its now clear the tariff rates are on the severe end of the anticipated outcomes. However, our initial view that severe tariffs might see initial USD strength and risk-off sentiment has not materialised, which we attribute to:

a) expectation for less severe implementation / off ramp

b) evolving market perception / confidence of the US

c) signs of fiscal tightening from Bessent

We note that this story is far from over, with the implementation schedule staggered throughout April and beyond, and potential for further negotiations in the coming days. This ongoing uncertainty adds to concerns around future US economic policy and could accelerate the reduction in overweight US positions from investors worldwide. EURUSD has rallied over 2% this morning (1.1101 at time of writing), perhaps reflecting repositioning in the EZ as a safe(r) haven, as well as a broader shift in sentiment towards the US.

Market impact

Although tariffs are on the higher end of expectations, the market seems more focused on growth implications rather than price effects, reflected in lower US interest rates in the medium to longer end. China is maintaining USDCNY despite the introduction of large tariffs (54%), whilst uncertainty surrounding the formula used for tariff calculation appears to be affecting market confidence in the US administration and the US safe haven / risk off mechanism traditionally seen. Treasury Secretary Bessent’s post-event communication highlighted fiscal tightening. While this may support the USD in the longer term, the near-term impact is less positive, particularly in comparison to fiscal expansion elsewhere.

After an initially muted reaction as the market digested the announcement, the dollar has weakened overall versus most major currencies. Along with the USD, US interest rates have fallen by around 8–12 bps in the medium to long end of the curve. This reflects concerns over US growth linked to tariffs, in tandem with the fiscal signals provided by Bessent. US S&P500 futures are approximately 3% lower following the announcement, with significant declines in companies reliant on international supply chains. These declines stem from higher import costs and continued uncertainty in policy direction.

Figure 1: DXY Index

Source: Bloomberg / Validus

Figure 2: EURUSD

Source: Bloomberg / Validus

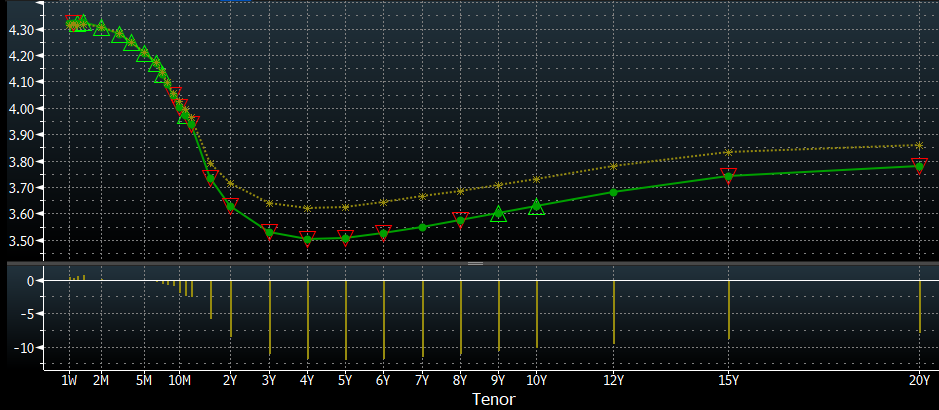

Figure 3: US Swap curve (latest versus Tuesday 1Apr25)

Source: Bloomberg / Validus

Figure 4: SP500 Jun25 Future

Source: Bloomberg / Validus

Where we go from here

Stagflation risk in the US has increased – we are likely to see a negative growth impact alongside price rises attributed to tariffs and supply chain disruption.

Real rates in the US have fallen; inflation is anticipated to be higher, and medium- to long-term nominal rates have declined. The upcoming US Nonfarm labour market report on Friday is viewed as the next key indicator.

It is challenging to determine whether the disruption to US growth will outweigh the price impacts and any ensuing need for higher short-term rates. Currently, the growth impact appears to dominate and the Fed may look through tariff driven price increases to support employment. Uncertainty remains over how much US equity weakness will be tolerated, given that domestic US consumers hold substantial equity positions and would be a political issue for Trump.

Overall, the US consumer appears increasingly vulnerable. Much of the wealth generated in the US exceptionalist era has not substantially filtered down to everyday consumers, prompting close monitoring of delinquency rates as an indicator. Still think there is a real risk of a US recession and substantial consumer credit / mortgage defaults.